Where to Invest: Dividend Growth Investing Or P2P Investing? (We Compare The Two Asset Classes)

What if your stocks increased in value over the years, and paid you money every month?

It’s possible.

In fact, there’s a name for it – dividend growth investing.

It’s a popular investment strategy that involves stocks, research and patience.

But how does dividend growth investing compare to P2P investing? And what’s the difference between these two strategies?

Let’s take a look at these two asset classes and compare them.

What is dividend growth investing?

Dividend growth investing is slightly different to stock market investing. With stocks, you buy, you hold them for a certain period of time, and then you sell (hopefully) at a profit.

Dividend growth investing turns stocks into a monthly income. How? Some company stocks issue dividends to their shareholders. These dividends are essentially paybacks on the profit that a company earns, like a bonus.

For example, Coca Cola pays out a dividend of $1.68 per share. That means that every quarter, you get $1.68 for every share of Coca Cola you own. Not only do you receive income, but you also hold that share — so in 20 years, you’ll also be able to sell Coca Cola stock (hopefully) for a profit.

It’s important to note that not every company does this.

Those that do, use dividends as an incentive so more people buy their shares. That means that if you want stocks to pay you a monthly income, you want to buy only from companies that issue decent dividends.

The magic of dividend growth investing happens when you choose to reinvest those dividends rather than take them out. By reinvesting, you are essentially buying more of your initial stock, and this helps grow your portfolio even bigger.

As time goes on, this helps accelerate the magic of compound interest. Not only that, but after 20 years, the value of your stock portfolio will also have increased. It’s a win-win!

A lot of dividend growth investors have a monthly income goal and try to reach it by investing in the right companies over time. Dividends are stable monthly income, and companies tend to increase dividends, so it’s a game of being patient and picking the right stocks.

The dividend growth investing mindset is: don’t time the market, pick a selection of high performing companies and stick with them.

Dividend investing vs P2P investing

So far, so good – right?

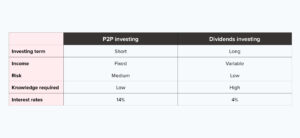

But how do the two investing strategies compare? Here’s a quick comparison:

Now, let’s take a closer look at how dividend investing compares with P2P investing.

1. Short term vs long term

One of the main differences between P2P lending and dividend growth investing are the time horizons.

P2P lending is more focused on short term returns. Depending on the platform, you won’t find loans that are more than a couple of years long. In Swaper’s case, our loans are 30 days long!

Your investments are short term, which is great for liquidity — but it means you need to continuously invest in order to make them long term.

Dividend growth investing is a completely different approach. It’s very long term, since stocks take a long time to accumulate and grow. The magic happens several decades in, when you’re earning dividends off your interest. That’s why it’s a strategy that works well for long term goals such as retirement or a pension.

2. Variable vs fixed income

One big benefit of dividend growth investing is that if a company becomes more successful and grows over time, then your dividends will increase as well. You’re investing in a growing business, and you can enjoy the benefits through dividends.

However, the opposite can also happen: companies can decide to stop paying dividends, and then you need to find another company to invest in. For example, Disney recently stopped paying out dividends due to the 2020 pandemic.

With P2P lending, the returns are usually fixed. You invest in a loan, and the borrower will pay interest every month. This amount is agreed beforehand and will remain the same until the loan term is complete. It means that the returns you get every month won’t increase or grow, but at least it means they won’t decrease!

3. Low risk vs medium risk

Dividend growth investing is considered very low risk. That’s because dividends are sent out from a company’s earnings (i.e. profit), which means the companies you are investing in are healthy and usually well established, such as Coca Cola, Disney, Johnson and Johnson, etc. Although they may stop paying out dividends, it’s incredibly unlikely that they will go bust.

Dividend-issuing companies are also listed on the stock market, which means their financials are published and they are easier to research.

P2P investing isn’t as risky as other asset investments such as cryptocurrencies, but it is considered more of a risk than dividend growth investing. That’s because you are lending money online, and it is possible for a borrower to default.

P2P loans aren’t as detailed, which can make it harder to do research and make investment decisions. The platform takes care of managing the loans, which is why it’s important to use a platform that is safe, secure and reliable.

4. Amount of research

Most dividend growth investors are passionate about dividends and companies, and love researching companies. That’s because in order to do this kind of investing properly, you need to be willing to do a lot of research, do the buying and selling yourself, as well as keep track of all your earnings. Dividend growth investing is the ultimate DIY investment.

What about with P2P lending? It’s a lot easier. You simply deposit your funds, set up auto invest and you’ll find yourself immediately investing in loans. Once you create an account, set up Auto-Invest and let the platform do the investing for you.

5. Interest rates

As an asset class, P2P investing does offer some of the highest returns — with Swaper, you can get 14%, or 16% with our bonus.

This isn’t the case with dividend growth investing. Dividend yields usually sit around 4% (dividend yield is how much a company pays in dividends relative to its stock price), and your stocks will generate an average of 8% per year.

These are still good returns, but they aren’t as high as with P2P lending. Most dividend growth investors are fine with that, since they mostly focus on passive income rather than yearly return. However, it’s still good to know.

Conclusion

Like stock market investing, dividend growth investing doesn’t exclude P2P lending as an investment.

In fact, the two investment types complement each other well: one is short term, the other long term. One is great for a monthly income, one is great for high returns.

Which should you pick? It mostly depends on your passions: if you don’t see yourself spending nights and weekends learning about how companies work, then P2P lending is good enough for you. But if you love investments and stocks, then dividend growth investing could be a fun “side-hustle”.

If you are diversifying your portfolio, it’s always good to have P2P investments as well as stocks.

So why not have stocks that also pay dividends? We believe both asset classes have a place in a well-diversified portfolio.

Ready to create an account with Swaper? Sign up today.