How Using a Credit Card Can Improve Your Credit Score

Expect the unexpected. Prepare for the unknown. In a vacuum, with unlimited resources – that would be the best strategy in order to avoid any financial struggles or delays. Then again – if you have unlimited resources, why in the world would you need to prepare for anything.

For those of us who don’t have access to unlimited funds, however, there may be another way…

Over the past few months, we’ve gone over multiple methods for reducing your debt and repaying loans in order to increase your wealth. However, there are various situations in life where an individual might find that it’s almost impossible to manage without borrowing funds. At the very least – the option to borrow often lets you achieve some goals much quicker than you otherwise would be able to. You have an urgent necessity to purchase an expensive home appliance, invest in your car’s repair or sudden health issues, that require additional funds, among other reasons. If you don’t have an emergency fund, if all your liquidity has been tied up in non-liquid assets, you may need to borrow.

Where does a (good) credit score come into play?

With that in mind, not everyone is entitled to a readily available loan. Especially, if you’ve never borrowed before OR you have borrowed – but it’s gone south for you somehow. In order to secure a loan, the lender you’re applying with will check your background – the most important of which is your credit score. If you’ve never borrowed before – you might not have a credit score at all. If you have borrowed and have experienced difficulties with making timely payments, repaying the loan or haven’t repaid it at all – it’s safe to say you DO have a credit score. Not one you would want to brag about.

Neither having a bad credit score or having none at all would immediately bar you from taking out a loan. However, it’s very likely that you would be offered much higher APRs and interest rates than otherwise with a good credit score. High APRs and interest rates in turn make these loans much more expensive. Even a 0.5 difference in mortgage interest could cost you tens of thousands of euros over the life of the loan. Similarly, with other, shorter term loans – a bad or non-existent credit score will cost you exponentially more than you could be paying with a better credit score.

So let’s see how you could improve your credit score or build one by using a credit card, shall we?

Why credit cards?

Well, it’s as simple as a credit card loan being on the lower side in terms of total amount as compared to other types of loans. Seems a little counterproductive to take out a mortgage or a student loan in order to improve your credit score, doesn’t it?

Getting yourself a credit card may initially reduce your overall credit score, as the lender will pull your credit score after receiving your application. This is temporary, however. As long as you make all your card payments on time, the credit score will increase again.

How does using the credit card help exactly?

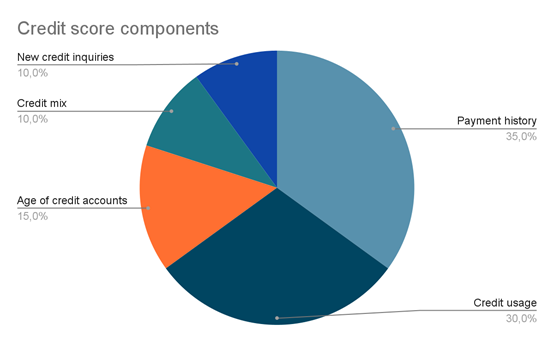

This also isn’t too complicated. For example, in the US a credit score is made up of five factors:

Europe does not have a unified credit score system, however most of the same components factor in your credit score.

The impact of each individual factor may also vary from country to country, or even loan provider to loan provider. What is more important for you, however, is how the use of a credit card can help mitigate this impact or even sway it to your favour. Here are some examples:

- Payment history

Making payments matters. Especially, making payments according to your loan schedule. This is one of the more typical reasons some people manage to utterly destroy their credit score. It’s unlikely a single late payment will do any lasting harm, but don’t make a habit out of missing your due date on payments – otherwise your credit score is bound to go down.

Make sure to pay at least the minimum required amount each scheduled period in order to maintain a good credit score. You can also repay the full credit card balance each month if your financial situation warrants it. If paying down a larger amount is too taxing for you, try and make two smaller payments each scheduled period – the minimum required, and then later in the period any amount you can afford. Not only will this help maintain and raise your credit score – the quicker you repay any loan, the less interest you pay in total.

- Credit usage

Credit usage is your credit utilisation ratio, or the amount of revolving credit you’re currently using divided by the total revolving credit available to you. Credit usage is usually expressed as a percentage. This factor ties in nicely with the previous – the quicker you repay your loan, the lower your credit usage, thus the higher your credit score.

Let’s say that you have a credit card with a credit limit of €8,000. You make a purchase of €2,000 with it. Your credit usage is now 25%. The rule of thumb with credit usage is to try and keep it under 30% when possible. That way, you would likely have both a good credit score and a chance to increase your overall credit limit.

- Age of credit accounts

This factor may not be as impactful for everyone around the globe – especially if you simply have not had the time to build a credit portfolio. But, credit companies do pay attention to the age of your credit accounts. The older your credit card account, the more favourably credit companies may look at you as a potential client (if you’ve maintained a good credit score, of course).

Do not close your older accounts unless absolutely necessary. By maintaining all your credit accounts, you both retain all your credit limits and maintain a stable credit score.

- Credit mix

Credit companies will also look at you more favourably if you ‘mix it up’. If you want to raise your overall credit score, but you don’t yet have a credit card account – get one. If you have multiple types of loans, both long-term and revolving (and you make sure to maintain a good credit score by keeping up with the payments) – credit companies will notice.

- New credit inquiries

This factor may seem a little counter-intuitive, but, if you want a better credit score – don’t ask for credit (as often).

Whenever you apply for a loan, be it a mortgage, car lease or a credit card, the credit company will make a so-called ‘hard inquiry’. Hard inquiries go on record, which means that if you, purposefully or otherwise, apply for multiple loans in a short period – credit companies will see that. Your credit score is likely to go down, as credit companies will view this as a sign of financial instability, therefore – a higher risk.

If you already have a less-than-desirable credit score, make sure you catch up on your payments or eliminate your debts entirely before applying for a new one. This way, you’re more likely to receive the loan you applied to, thus reducing the chance of multiple new inquiries.

In conclusion

You don’t necessarily have to have a credit card to have a good credit score. The most important factor still is taking care of your payments with any loan you might have. Don’t be late (rare occasions are acceptable, as long as you catch up as soon as possible).

If you do decide to use a credit card, do so accordingly. Pay your bills and maintain a lower credit utilisation ratio. Don’t close down on your older credit cards, as it could be counter-productive towards your credit limit. With proper usage, your credit score will go up, not down.

This is an informative blog entry and should not be taken as financial advice.